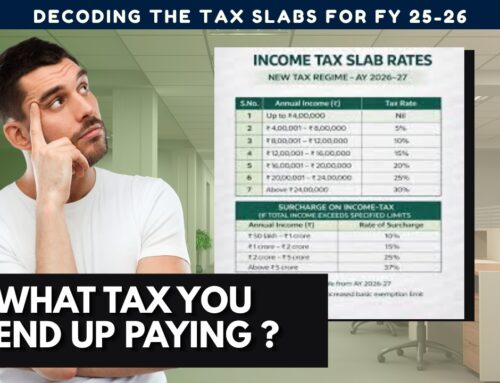

TL;DR

While AI and robo-advisors have revolutionized financial planning through automated portfolio allocation, speed, and cost efficiency, they often fall short during periods of high emotional stress. Technology excels at logic-based optimization, yet it cannot provide the empathy, judgment, or behavioral coaching necessary when market volatility triggers fear and impulsive decision-making

Fee-only human advisors act as fiduciaries, offering unbiased guidance that considers a client’s unique life context beyond mere data points. While robo-advisors are suitable for beginners with simple needs, human intervention becomes critical as financial complexity and investment sizes increase. Ultimately, the ideal approach to long-term success in the AI era combines technological efficiency with human insight, ensuring investors remain disciplined and aligned with their goals amid uncertain market cycles.

On a quiet evening in Pune, Neha opened her investment app and stared at her portfolio. Markets had fallen sharply over the past few weeks. News channels were talking about global uncertainty. Social media was full of conflicting opinions.

She had recently started using a robo-advisory platform. It looked efficient. It rebalanced her portfolio automatically. It sent alerts. It showed projections.

Everything seemed logical. But that evening, logic was not her problem. Fear was.

She wondered, “Should I stop my SIPs? Should I reduce equity? What if this time is different?”

The app did not answer.

It is where the real conversation about financial advice begins in 2026.

The Rise of Robo-Advisors and AI in Financial Planning

Over the last decade, financial technology has transformed how individuals invest. Robo-advisors and AI platforms now offer:

- Automated portfolio allocation

- Goal-based investing models

- Tax optimization suggestions

- Rebalancing without human intervention

Tools powered by artificial intelligence, including platforms similar to ChatGPT and Google Gemini, can process vast amounts of financial data within seconds.

They can:

- Simulate retirement scenarios

- Compare investment strategies

- Optimize asset allocation

- Calculate risk metrics

From a computational perspective, AI has become incredibly powerful. For many investors, this raises an important question. If technology can do all of this, do we still need a human financial advisor?

Before we compare, it is important to acknowledge that robo-advisors bring significant value.

Data Processing and Speed

AI systems can analyze thousands of data points instantly.

They can:

- Calculate optimal portfolios

- Adjust allocations based on risk

- Run simulations for different scenarios

This level of speed and efficiency is unmatched.

Cost Efficiency

Robo-advisory platforms are often low-cost.

They reduce:

- Advisory fees

- Human intervention

- Operational overhead

It makes them accessible to a wider audience.

Discipline Through Automation

One of the biggest advantages is the removal of manual intervention.

Automated systems can :

- Rebalance portfolios regularly

- Continue SIPs without emotional interruption

- Follow predefined rules

It reduces impulsive decision-making to some extent.

Where Robo-Advisors Fall Short

Now let us return to Neha’s situation. Her portfolio was designed well. Her asset allocation was appropriate. Her long-term goals were clear. Yet she felt anxious.

Why?

Because financial planning is not just mathematical, it is deeply human.

Handling Emotions During Market Volatility

Markets do not test your intelligence. They test your behavior. During a market fall, investors experience:

- Fear of loss

- Regret

- Uncertainty

- Panic

An AI system can tell you:

“Stay invested for long-term growth.”

But it cannot sit across the table and understand:

- Your anxiety

- Your family situation

- Your past experiences with money

A human advisor can.

Context Beyond Numbers

AI works on inputs. But life is not always structured. Consider situations like:

- Sudden job loss

- Health emergencies

- Family responsibilities

- Business risks

These are not just financial variables. They are personal realities. A human advisor interprets numbers in the context of your life.

Behavioral Coaching

One of the most underrated roles of a financial advisor is behavioral coaching. Studies across global markets have shown that investor returns are often lower than market returns due to poor decisions, such as:

- Exiting during market falls

- Chasing trends

- Timing the market

A human advisor helps you stay aligned with your plan. It is not about giving advice. It is about guiding decisions.

Fee-Only Advisors: What Makes Them Different

A fee-only financial advisor operates on a simple principle. They charge a transparent fee for advice and do not earn commissions from products. It creates an important alignment. Their focus remains on:

- Your financial goals

- Your risk capacity

- Your long-term outcomes

Not in selling financial products.

Why This Matters in the AI Era

In a world where information is easily available, trust becomes more important than access. AI can provide information. But it cannot build trust. A fee-only advisor:

- Acts as a fiduciary.

- Prioritizes client interest.

- Provides unbiased advice

It becomes critical when financial decisions involve large sums and long time horizons.

The Real Difference: Logic vs Judgment

Let us simplify the comparison.

Robo-Advisor

- Strength: logic

- Focus: optimization

- Approach: rule-based

Human Advisor

- Strength: judgment.

- Focus: decision making

- Approach: contextual

Financial planning requires both. But in moments of uncertainty, judgment often matters more.

A Story of Two Investors

Let us consider two individuals.

Investor A: Fully Automated

- Uses a robo-advisor.

- Portfolio is well designed.

- During a market fall, panic sets in.

- Stops SIPs.

- Reduces equity allocation.

- Misses market recovery.

Investor B: Guided by Advisor

Has a similar portfolio. During the same market fall, speak with an advisor. Understands:

- Market cycles.

- Long-term perspective.

- Personal risk capacity

Continuous investments.Benefits from recovery. The difference is not intelligence. It is guidance.

Can AI Replace Financial Advisors?

This is the question many people are asking. The realistic answer is nuanced. AI will transform financial advisory. But it will not replace it.

What AI Will Replace

- Basic calculations

- Standard portfolio allocation

- Data analysis.

- Reporting

What AI Cannot Replace

- Empathy

- Judgment

- Accountability

- Trust

- Behavioral coaching

These are human elements. And they become more valuable during uncertainty.

The Ideal Approach: Human + Technology

The future is not about choosing between AI and human advisors. It is about combining both. A strong financial advisory model uses

- Technology for efficiency

- Human insight for decision making

It creates:

- Better planning

- Faster execution

- Stronger client relationships

Why This Matters for Long-Term Financial Planning

Financial planning is not a one-time activity. It is a long-term journey that involves:

- Changing goals.

- Evolving income.

- Life transitions.

- Market cycles

Over 20 to 30 years, your plan will need adjustments. AI can assist. But it cannot lead.

Who Should Rely Only on Robo-Advisors

There are cases where robo-advisors can work well. For example:

- Beginners with small investments

- Individuals with simple financial situations

- Those who are comfortable with market volatility

Who Needs a Human Advisor

A human advisor becomes important when:

- Financial goals are complex

- Investment size increases.

- Retirement planning becomes critical

- Emotional decision-making becomes a risk

The Cost Question

One of the biggest concerns people have is cost. Robo-advisors are cheaper. Human advisors charge fees. But the real question is not cost. It is valuable. If an advisor helps you:

- Avoid major mistakes

- Stay invested during volatility

- Align investments with goals

The long-term benefit can be significantly higher than the fee.

Bringing It Back to Neha

Neha eventually spoke with a financial advisor. Not to redesign her portfolio. But to understand her emotions. The advisor explained:

- Market corrections are normal

- Her goals are long-term

- Her allocation is appropriate

More importantly, the advisor helped her stay invested. That decision mattered more than any algorithm.

The Bottom Line

Robo-advisors and AI have made financial planning more accessible and efficient. They are valuable tools. But financial planning is not just about numbers. It is about people.

It is about:

- Fears during uncertainty

- Discipline during volatility.

- Clarity during complexity

And these are areas where human advisors play a critical role.

Final Thought

In the AI era, the question is not whether technology will change financial planning. It already has. The real question is:

Who will guide your decisions when markets are uncertain, and emotions take over?

Because in those moments, the most valuable asset is not data.

It is perspective.

Disclaimer

This article is for educational purposes only and should not be considered financial advice. Investment decisions should be made based on individual financial goals, risk tolerance, and professional consultation.

NS Wealth is a top SEBI-registered investment advisory company in India. and Provide Financial Planning Across the City in India: Bhubaneswar | Delhi NCR | Bangalore | Hyderabad | Kolkata | Chennai | Nagpur | Nashik | Pune | Mumbai | Jaipur | Indore | Ahmedabad