First Published on Mint

For Pratibha Jadhav, the journey toward financial independence began with a lesson inherited from her father: the importance of a consistent saving habit. While many of her peers struggle with heavy EMI burdens and a lack of retirement planning, Jadhav has prioritized financial security from the start of her career.

The Investment Strategy

Jadhav’s portfolio is built on a foundation of diversification and professional guidance. Introduced to NS Wealth Solution, a SEBI-registered investment advisor (RIA), she transitioned from parking funds in fixed deposits to actively managing mutual funds.

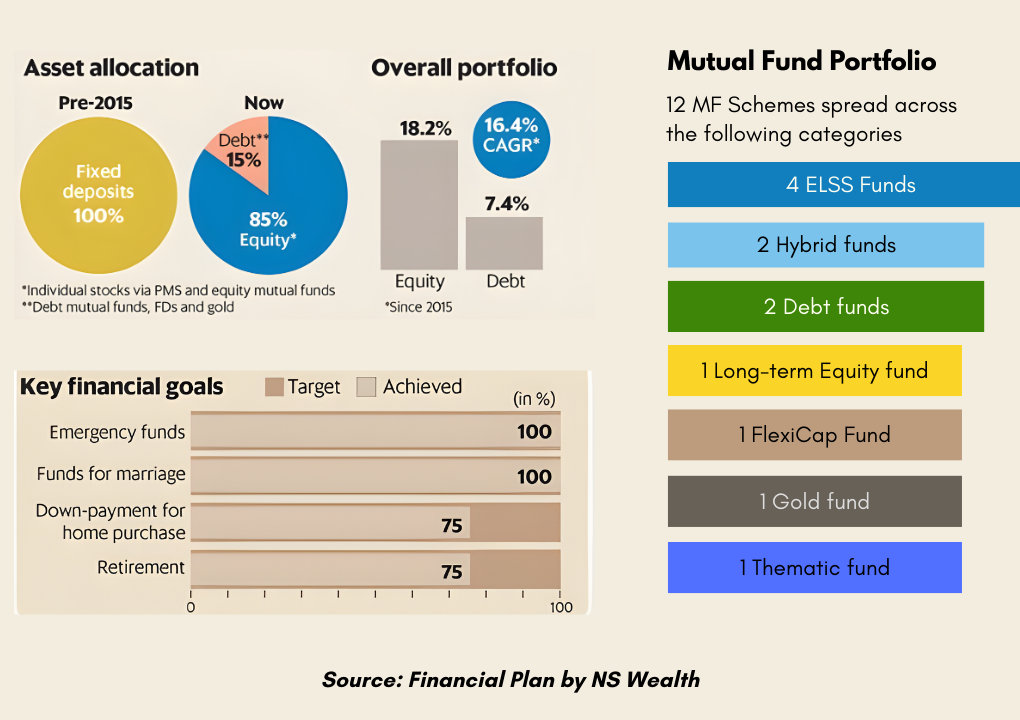

Her current portfolio, which consists of 12 mutual fund schemes across large-cap, hybrid, flexi-cap, and liquid funds, has delivered impressive results:

- Total Portfolio CAGR: 16.4% since inception.

- Equity Portion: 18.2% CAGR.

- Debt Portion: 7.4% CAGR.

To manage what might seem like a “cluttered” portfolio, her advisor, Nagraj Fakira Pawar, uses quartile analysis. Every quarter, funds are ranked by performance, cost, and valuation. Fresh SIP (Systematic Investment Plan) contributions are directed into the top-performing funds in the first quartile, while existing funds are only exited if they fall to the bottom quartile.

Beyond mutual funds, Jadhav took advantage of the March 2020 market crash to invest in fundamentally strong stocks and eventually moved into a Portfolio Management Service (PMS) tailored to her risk appetite

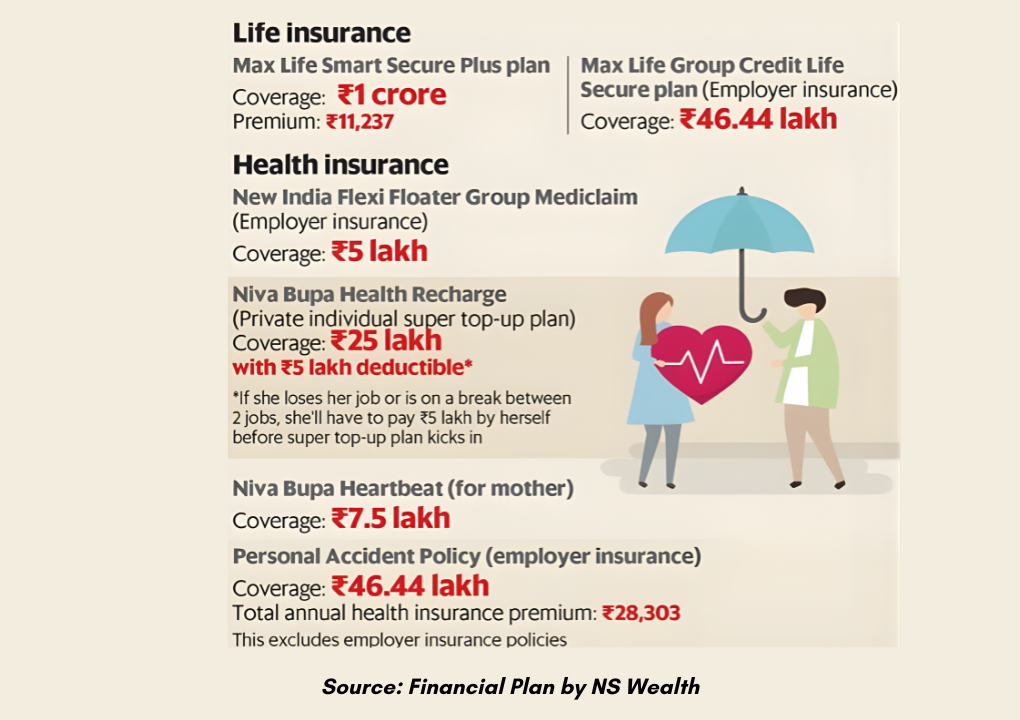

Comprehensive Insurance Protection

A key pillar of Jadhav’s financial plan is her robust insurance coverage, blending employer benefits with private policies.

The super top-up plan acts as a cost-effective safety net. While her employer’s policy covers the ₹5 lakh deductible, the top-up ensures she is protected even if she switches jobs or faces a major medical emergency.

Goal-Based Planning and Fees

Jadhav maintains high liquidity, keeping two months of salary in savings and the rest in investments or emergency funds (FDs and liquid funds). Having already achieved her savings goal for her marriage, she is now focused on a down payment for a home and her retirement. Currently, she has achieved 75% of the future value needed for these long-term goals.

To maintain this growth, she utilizes a transparent fee-based advisory model:

- Advisory Fee: 1% of Assets Under Advisory (AUA) or a minimum of ₹1,500 per month.

- PMS Fee: 2% annually (split between the advisor and the PMS provider).

- Onboarding: A one-time fee of ₹10,000 for the first three months.

As Jadhav prepares for marriage, her commitment remains firm. She plans to align goals with her future husband while keeping their individual investments separate to maintain the discipline that has brought her this far.

Key Takeaways

- Start Early: Structured planning is the primary driver of growth.

- Diversify: Spreading investments across asset classes maximizes returns.

- Review Regularly: Use strategies like quartile analysis to ensure your funds remain competitive.

Planning is the first step towards building a strong financial future, and talking to a Certified Financial Planner is the way forward.